Greater China—mainland China, Taiwan, Hong Kong, and Macau—has been one of the fastest-growing licensing markets within Asia and in the world over the past few years. In fact, two of the countries in Greater China, the mainland and Macau, were the first and second fastest-growing individual countries in retail sales of licensed products in 2013, with increases of 9.2% and 9.0%, respectively, according to The Licensing Letter’s “International Licensing: A Status Report.” Given recent upward revisions of GDP growth for China, the trend is likely continuing.

Together, the countries of Greater China saw an increase of 8.3% in retail sales of licensed goods in 2013, and a two-year gain of 17.0% from 2011 to 2013. Total retail sales of licensed merchandise in Greater China in 2013 approached $6.4 billion.

The countries within Greater China are very different from one another when it comes in their licensing landscapes. Most notably, Taiwan and Hong Kong are better established, so per-capita sales are higher ($21.74 and $40.35, respectively, compared to $4.07 for mainland China), but their greater maturity and lower populations mean growth prospects are lower.

Even as mainland China’s licensing market is still considered emerging, it is already the sixth-largest single country in total retail sales of licensed goods. With $5.5 billion in retail sales, it falls behind only the U.S., Japan, Canada, the U.K., and France in this ranking.

That said, while some licensors are doing well in the mainland, most still are dealing with a steep learning curve and the many challenges that the business faces in this market. The rest of the countries in the region, while smaller, are easier to navigate.

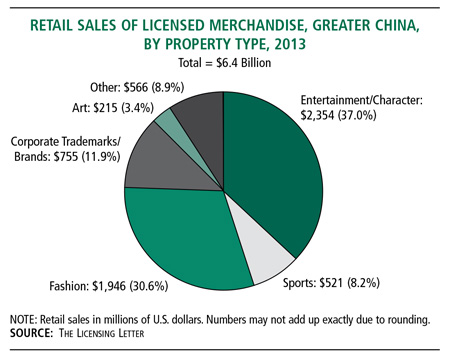

Sales by Property Type

Entertainment/character licensing drives 37% of retail sales of licensed goods in Greater China, the largest sector in the territory, followed by fashion with a 30.6% share. The two segments were the first to be established in mainland China. Within entertainment/character sector, properties from Disney and other major licensors in the U.S., and Japanese and European licensors, continue to maintain a strong share. Disney was one of the first U.S. studios to establish itself in this market and continues to grow, but still attributes to China a relatively small portion of sales. Increasingly, IP from Japan, South Korea, and Greater China itself is being introduced here. Xi Yang Yang, or Pleasant Goat and Big Big Wolf, is just one property from mainland China that has made a real mark at retail, while properties from Hong Kong and Taiwan also have begun to emerge.

In fashion, competition from local properties—often known only in China—is a challenge, with examples including apparel retailer Metersbonwe and outerwear brand Bosideng, among many others. But global fashion labels, especially from Europe and, to a slightly lesser degree, the U.S., continue to be in demand.

Global fashion designers frequently enter the market with their own stores. Phillips-Van Heusen licensed Dishang to operate its IZOD stores in Greater China in 2011, anticipating a total of 1,000 points of sale ultimately, including at least 500 freestanding stores as well as shop-in-shops.

Other smaller, but recently growing, property types include corporate trademarks/brands with an 11.9% share of market in 2013, sports with an 8.2% share, and art with 3.4%.

All the major property types grew at double-digit rates from 2011 to 2013 in Greater China.

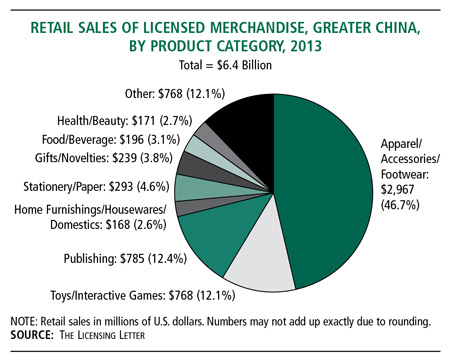

Sales by Product Category

Apparel, accessories, and footwear account for nearly half (46.7%) of all retail sales of licensed goods in the region, followed by publishing with 12.4%. The latter is sometimes used by foreign entertainment/character properties to gain a foothold in mainland China, both with retail books and magazines and with educational materials for schools.

Toys and interactive games round out the top three categories, with a 12.1% share of market. But the range of licensed products and services in Greater China is vast, especially for a relatively undeveloped market. Examples range from licensed Fiat cafés in Hong Kong (location-based licensing is a growth area in general) to Hello Kitty fruit- flavored beer in the mainland. And luxury goods across all categories and property types are growing. Credit and debit cards also are popular, featuring licenses from Tom & Jerry to LINE Friends.

Every product category saw an increase in retail sales in Greater China from 2011 to 2013. Wearables, already by far the largest category, saw the fastest rate of growth by a wide margin—the sector was up 25.2% during the two-year period—another indication that this market is still emerging.

Food/beverage and health/beauty were the next fastest-growing categories, rising 15.2% and 14.2%, respectively.