- EIU predicts greater drop in global GDP

- Consumer confidence plummets

- IMF predicts gas embargo by Russia could further impact EU economy

- Licensed consumer sales predicted to drop in late 2022 and throughout 2023

By Gary Symons

TLL Editor in Chief

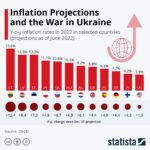

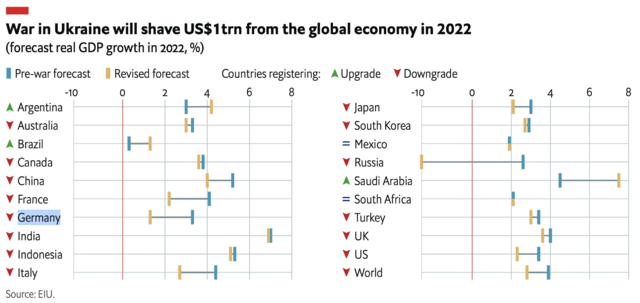

More gloomy news for the licensing industry as the Economist Intelligence Unit predicts the War in Ukraine will shave $1 trillion from the global economy in fiscal 2022.

Prior reports in The Licensing Letter have combined our own survey and data research along with analysis of reports by the IMF, World Bank, and other economic organizations, all of them pointing to a major retraction in economic activity at the global level.

The EIU report, however, is the first we’ve seen to put a dollar figure to the expected reduction in global economic GDP.

“The war in Ukraine is affecting the global economy via higher commodity prices, supply-chain disruptions and worsening sentiment for both households and businesses,” concludes the EIU’s Global Economic Outlook 2022. “These three factors are causing global inflation to spike and growth to slow.”

“The war in Ukraine is affecting the global economy via higher commodity prices, supply-chain disruptions and worsening sentiment for both households and businesses,” concludes the EIU’s Global Economic Outlook 2022. “These three factors are causing global inflation to spike and growth to slow.”

The issue for the licensing and consumer products industries is that the War in Ukraine is causing disruptions in the supply chain for critical products, including food, oil and gas. These disruptions are causing prices for the most basic commodities to soar, driving up inflation globally, and even creating the risk of mass starvation in many less affluent countries.

Creator: Uwe Aranas Copyright: © by CEphoto, Uwe Aranas

Creator: Uwe Aranas Copyright: © by CEphoto, Uwe Aranas

EU Further Threatened by Potential Russian Gas Embargo

Even as that news sinks in, alarm bells are ringing across Europe as the IMF warns several EU nations may be hit by a complete shutdown of Russian gas supplies, because Russian President Vladimir Putin is expected to retaliate for Western sanctions. It’s believed the Kremlin also wants to shake NATO’s resolve to support Ukraine by hitting citizens in the EU with energy rationing and a downturn in the economy.

If that happens, the IMF says Hungary, Slovakia and the Czech Republic will be hardest hit, potentially seeing a drop in GDP of 6%, but the move would also cause severe impacts for Germany, Italy and Austria.

“The prospect of an unprecedented total shutoff is fuelling concern about gas shortages, still higher prices, and economic impacts. While policymakers are moving swiftly, they lack a blueprint to manage and minimise impact,” IMF officials said in a blogpost.

“Our work shows that in some of the most-affected countries in Central and Eastern Europe, there is a risk of shortages of as much as 40% of gas consumption and of gross domestic product shrinking by up to 6%.

“Our work shows that in some of the most-affected countries in Central and Eastern Europe, there is a risk of shortages of as much as 40% of gas consumption and of gross domestic product shrinking by up to 6%.

“The impacts, however, could be mitigated by securing alternative supplies and energy sources, easing infrastructure bottlenecks, encouraging energy savings while protecting vulnerable households, and expanding solidarity agreements to share gas across countries.”

Unfortunately, the War in Ukraine is not the only headwind facing the global economy. The EIU also cites the impact of China’s zero-COVID policies, which have seen factories, ports, and even entire cities shut down after relatively small outbreaks of COVID-19.

“China’s zero-COVID policy is another major drag on global growth, and we expect it to continue well into 2023,” the EIU states. “In addition, we now believe that China’s fiscal stimulus measures will have less of a positive impact than previously expected. The combination of these factors will weigh severely on China’s growth, which we now forecast to be no higher than 4% this year (well below our previous forecast of 5% and a government target of 5.5%).

“Beyond stringent lockdowns and curbs on domestic and foreign travel, China’s increasingly ideological stance on COVID-19—coupled with our expectation that sudden shutdowns of other Chinese cities will recur throughout 2022—will continue to weigh on global sentiment this year.”

The domino effect of inflation and disrupted logistics is causing a decline in consumer confidence, which The Licensing Letter covered in our most recent TLL Annual Licensing Sales Report, subtitled “War, Pandemic and Famine Threaten Licensing Recovery.”

(Subscribers can access that report in the July magazine HERE.)

Among many other problems facing the licensing industry is that consumer confidence plummeted to its lowest point since the stock market and sub-prime mortgage crash that touched off the Great Recession in 2008-2009. In fact, consumer confidence now has sagged lower than at the height of the panic over the COVID-19 pandemic.

While the pandemic appears to be slowly drawing to a close, the EIU is not optimistic about a timely end to the Ukraine crisis, which echoes the predictions of military analysts in the US and the UK.

While the pandemic appears to be slowly drawing to a close, the EIU is not optimistic about a timely end to the Ukraine crisis, which echoes the predictions of military analysts in the US and the UK.

“This situation will continue over the rest of the year,” the report predicts. “EIU expects the war to last until the end of 2022 at least, before settling into a protracted stand-off with periodic flare-ups.”

That’s obviously very bad news for the people of Ukraine, but also means the effects of the Russian invasion will continue to impact the global economy.

Primary among those effects are, first, the Russian blockade of Ukrainian ports and the mining of sea lanes in the Black Sea, which has hampered the country’s ability to export wheat, and second, the creation of oil and gas shortages for European members of NATO.

For this reason, while the war will create downward pressure on all economies, the EIU says the situation will be quite different in various regions, depending upon their reliance on Ukrainian grain shipments and/or Russian oil and gas.

For example, Brazil and Argentina are expected to suffer little from the conflict, particularly as Brazil has signed a deal to buy massive quantities of Russian oil products at a reduced price per barrel. Those two countries have actually seen an upgrade in their expected GDP for the year.

Similarly, oil producers like Saudi Arabia are doing just fine, with that country’s GDP upgraded from to grow from 4.2% to more than 7% this year thanks to higher oil prices. Notably, Saudi Arabia just turned down a request from the United States to increase oil production, which would have lowered oil prices and help Europe stave off potential energy restrictions this winter.

Europe To Face Long-term Consequences of Dependence on Russian Energy Imports

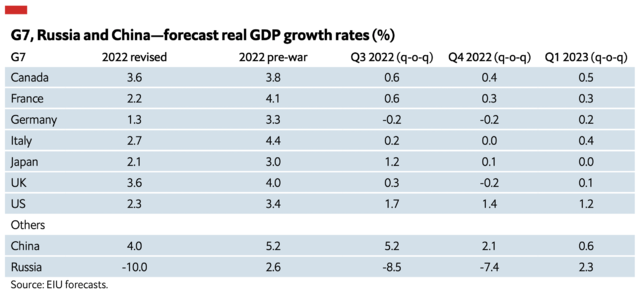

However, the EIU has downgraded expectations for most countries in the region, with Russia leading the downward spiral. Prior to the war Russia was expected to enjoy GDP growth of around 2.6%, but the EIU now expects Russia’s economy to shrink by 10% in what is essentially a self-inflicted recession.

Other than Ukraine and Russia, Europe is the region expected to be most directly impacted by the War in Ukraine, and also by logistics wrangles in China.

“European economies are facing three simultaneous headwinds,” the EIU report summarizes. “Surging inflation is weighing on consumers’ purchasing power and damaging business sentiment; external demand is slowing as the US tightens monetary policy and China continues its zero-COVID policy; and spillover effects from the war in Ukraine are dampening growth via higher commodity prices and disrupted supply chains.

“Germany will be particularly affected by these factors; we now expect the country to be in a technical recession (two consecutive quarters of negative growth) in the second half of this year,” the report adds.

In fact, that prediction may now be optimistic, due to fears Russia may turn off the taps for oil and gas exports to Germany, which would cause deep rationing of fuel, and could even cause industrial output to drop significantly. That country is not only deeply reliant on Russian oil and gas imports, but is also continuing with its long-held plans to shut down nuclear plants despite the energy crisis—a decision that has perplexed some EU partners.

Most of the other EU economies will likely do better, thanks to a low reliance on Russian energy.

“We still expect real GDP in the euro zone to return to its pre-pandemic level on average in 2022,” the EIU says. “However, Russia’s invasion of Ukraine has prompted us to almost halve our forecast for growth in the bloc this year, to 2.2% (from a pre-war forecast of 4%).

“In addition, headline growth figures for 2022 will be misleadingly positive. Carry-over effects in the first quarter of 2022 from strong growth in 2021 mean that, even with zero quarterly growth in the remainder of the year, most euro zone economies will register strong annual growth rates this year. Conversely, minimal carryover effects from 2022 mean that growth will slow in 2023.”

Right now, that actually looks like a best case scenario. As noted above, the IMF’s alarming declaration on the economic impacts of a total shutdown of Russian gas supplies would drag those numbers down significantly.

In the event of a total shutdown, the IMF predicts the EU as a whole could suffer a drop in economic output of almost 3% over the next 12 months.

Some countries, such as Sweden, Denmark and Greece, would see little or no impact on growth, but Italy could suffer a hit of more than 5% due to its high reliance on gas for generation of electricity.

“The effects on Austria and Germany would be less severe but still significant, depending on the availability of alternative sources and the ability to lower household gas consumption,” the IMF said.

Lowered Expectations for US Economy

The United States is not dependent on Russian energy, but it is being affected by rising food and energy costs, the ongoing logistics crisis, and a loss of confidence among both consumers and investors. With the stock market seeing a major decline this year and the cost-of-living rising sharply, the EIU is predicting a pull back in spending and economic activity.

The United States is not dependent on Russian energy, but it is being affected by rising food and energy costs, the ongoing logistics crisis, and a loss of confidence among both consumers and investors. With the stock market seeing a major decline this year and the cost-of-living rising sharply, the EIU is predicting a pull back in spending and economic activity.

Fortunately, the EIU does not expect the country to fall into a full recession.

“In the US, economic warning signs started to flash in early 2022, raising concerns that the country’s economy could be headed for a recession,” the report says. “After a sharp economic rebound in 2021, real GDP contracted at an annualized rate of 1.6% in the first quarter of 2022. Despite strong domestic demand, the war in Ukraine sent energy prices soaring and China’s zero-COVID policy weighed on exports by exacerbating supply-chain issues.”

The EIU has lowered GDP expectations to 2.3% this year, down from a pre-war forecast of 3.4%.

“We expect consumer demand to be sufficiently resilient to avoid an outright recession, thanks in part to the tight labour market and strong household balance sheets,” the EIU predicts. “However, this does not mean that a US recession is not a significant risk.

“Three triggers could prompt an economic contraction later this year or in 2023: a sudden spike in inflation (for instance if the situation in Ukraine deteriorates), an overly aggressive Federal Reserve (the US central bank), and a collapse in asset prices.”

Potential Catastrophe Threatens Developing Economies

Those two countries are among the top 10 wheat producers in the world, and supplies from both have dwindled due to the war. Ukraine in particular is expecting to see its wheat imports crash to just 30% of normal, leaving some countries scrambling to secure food imports.

In particular, NATO member Turkey is very dependent on Russian and Ukrainian wheat imports, getting more than 70% of its supply from those countries.

The same is true in Egypt, Lebanon, Benin, the Congo, Mongolia and Nicaragua.

Many other countries, most of them in Africa, are also heavily dependent on Ukrainian and Russian wheat, comprising anywhere from 40 to 70% of their annual supply. For these countries, the threat from the war goes far beyond rising prices, creating the very real possibility of mass starvation for up to 50 million people. In the face of soaring prices in Africa for the basic necessities of life, spending on consumer products is expected to see a major decline through 2023, barring an early end to the war.

How Could the Situation Change?

As Russia has opted for a long, drawn-out scorched earth strategy in its attack on Ukraine, both military and economic analysts have concluded the war is very likely to last through 2023, and so the economic impacts will continue for years to come.

However, there are a number of ways the situation could rapidly change, for better or for worse.

Some military analysts now believe Russia’s threats of nuclear retaliation are a bluff, and that the Kremlin won’t risk a nuclear exchange that would destroy the country. A minority are even advocating that NATO should enter the war on the side of Ukraine, and use its much greater military weight to put a rapid end to the conflict.

A larger number are calling on NATO to pull out all the stops on supplying weapons and training new Ukrainian troops, and that is beginning to happen. Ukraine is getting more advanced weapons, including long-range rocket and artillery systems, tanks, and even fighter jets from the US. Combined with training programs, such as one in the UK training 10,000 soldiers at a time, it is possible that Ukraine will reach its goal of creating a million soldier army and will be able to drive Russia out of the country by December, as President Volodymyr Zelensky has claimed is possible.

A third option that could improve the global economic outlook would be if NATO intervened to escort grain shipments from Ukrainian ports, as Turkey has called for.

That would not solve the energy shortage in Europe, but it would greatly reduce global food prices and overall inflation.

On the other side of the coin, however, it is also possible that Russia may escalate the conflict, cutting off all oil and gas supplies to Europe, and doubling down on its blockade of food exports. This week the Russian Army has begun shelling the Black Sea port of Mykolaiv, which some analysts believe is a prelude to a Russian attempt to take the entire Black Sea coastline, and permanently shut down Ukrainian wheat exports by sea.

The EIU, however, believes the most likely outcome given the battered state of both country’s militaries is a long and costly war of attrition that will continue to drag on the global economy through the end of 2023.

TLL Special Report: War, Pandemic and Famine Threaten Licensing Recovery

Twin Studies Predict Strong Recovery For Licensing and Retail